Published as part of the ECB Economic Bulletin, Issue 8/2024.

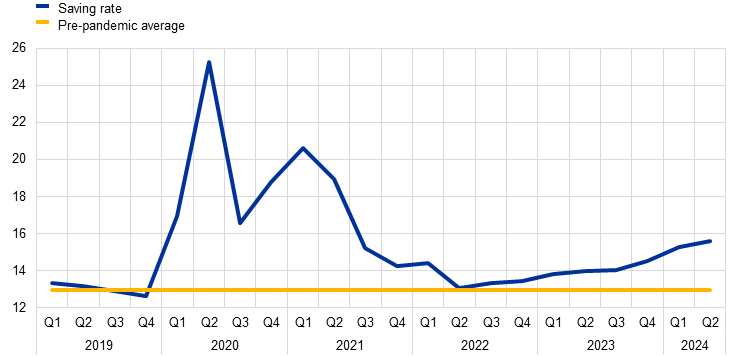

Following a pandemic-related surge in 2020, the household saving rate in the euro area fell back to its pre-pandemic average by mid-2022 but has since risen again noticeably. The seasonally adjusted euro area household saving rate, as reported by Eurostat in the quarterly sector accounts, rose sharply after the outbreak of the COVID-19 pandemic.[1] This was mainly due to the lockdowns imposed to contain the spread of the virus, which dampened consumption, while government measures helped to support disposable incomes.[2] With the restrictions largely lifted by 2022, the saving rate returned to its pre-pandemic average (Chart A). It has, however, increased again over the last two years, while consumer spending has remained sluggish. This box analyses the main economic factors behind this recent rise in the saving rate and explores the near-term implications for private consumption.

Chart A

Household saving rate

(percentage of gross disposable income)

Sources: ECB and Eurostat (QSA) and ECB calculations.

Notes: Seasonally adjusted data. The pre-pandemic average is computed from the first quarter of 1999 to the fourth quarter of 2019.

Strong income growth has contributed to the recent increase in the household saving rate. Real household income has increased by 3.8% over the last two years, thanks to strong growth in both labour and non-labour components (Chart B). The increase in non-labour income, which includes income from self-employment, net interest income, dividends and rents, is particularly favourable for savings.[3] This reflects the fact that non-labour income mainly accrues to richer households, who generally save more than poorer households.[4] In addition, fiscal policy has also supported real income growth since the third quarter of 2022. This can be largely attributed to the discretionary measures to mitigate the impact of the energy price shock, including substantial non-targeted income support. Since richer households have also benefited from the measures and consume a smaller share of their income, this may also have contributed to a higher saving rate.[5]

Chart B

Developments in real household income

(percentage changes since the second quarter of 2022 and percentage point contributions)

Sources: Eurostat, ECB and Eurostat (QSA) and ECB calculations.

Notes: Seasonally adjusted data. Labour income is calculated as compensation of employees and non-labour income includes income from self-employment, net interest income, dividends and rents; fiscal income is measured as a residual. To obtain real values, all household income components are deflated using the private consumption deflator from the national accounts.

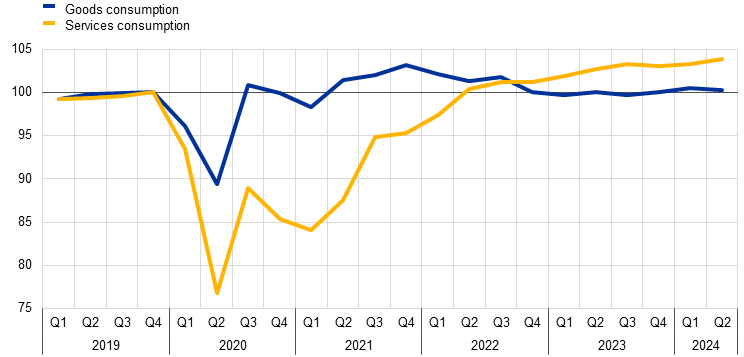

Although their income has risen strongly over the last two years, households have remained cautious about their spending. Following a post-pandemic rebound, real private consumption growth weakened markedly in the context of surging inflation and the subsequent tightening of monetary policy. The rise in inflation was driven in large part by a strong increase in energy and food prices, which led to a relatively sharp decline in the consumption of these goods.[6] The subsequent increases in interest rates encouraged saving and likely dampened the consumption of goods more than the consumption of services. The consumption of durable goods was particularly affected, as it is more sensitive to interest rates than services are.[7] Overall, consumption of goods fell back below its pre-pandemic level at the beginning of 2023 and has largely stagnated in the last two years. At the same time, consumption of services has continued to rise, but at a more moderate pace (Chart C).

Chart C

Real household consumption of goods and services

(Q4 2019 = 100)

Sources: Eurostat and ECB calculations.

Notes: Seasonally adjusted data. Goods consumption and services consumption are based on the aggregation of available data on real household consumption by purpose.

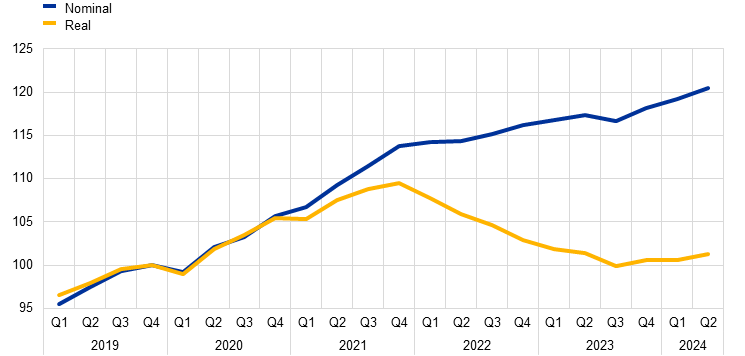

With the surge in inflation, households’ real net wealth declined in the past two years, increasing the incentives for them to rebuild their wealth. The net wealth of households, which includes real estate assets, deposits, bonds and shares, minus debt liabilities, rose significantly in the wake of the pandemic, supported by the accumulation of pandemic-related savings. It continued to increase after the pandemic in nominal terms, albeit at a more moderate pace (Chart D).[8] In real terms, however, household net wealth began to decline in 2022 and fell back to its pre-pandemic level in the course of 2023. This decline has likely contributed to the recent increase in the household saving rate, as households have been incentivised to rebuild their real net wealth.[9]

Chart D

Household net wealth

(Q4 2019 = 100)

Sources: Eurostat, ECB and Eurostat (QSA) and ECB calculations.

Note: To obtain real values, household net wealth is deflated using the private consumption deflator from the national accounts.

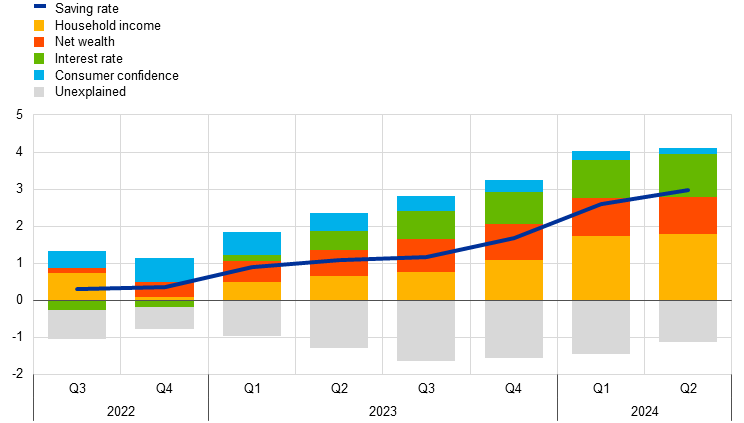

A time-series model for household consumption using standard macroeconomic determinants helps to shed more light on the economic factors behind the recent increase in the saving rate. A reduced-form error correction model combines both long-term and short-term dynamics to explain quarterly consumption growth.[10] The level of real household consumption is driven in the long term by the level of real household income, the real net wealth of households and real interest rates. In the short term, other cyclical factors, such as consumer confidence which reflects precautionary saving motives, also play a role in explaining consumption dynamics. The model decomposes the change in the household saving rate into four factors – income, wealth, interest rates and consumer confidence – taking growth in real household income as given.[11]

Empirical evidence suggests that rising real incomes and high real interest rates, together with negative real wealth effects, have pushed up household savings over the past two years. According to the model results, the increase in the household saving rate between the second quarter of 2022 and the second quarter of 2024 can be largely attributed to income effects, as households’ consumption did not adjust immediately to the strong rise in real incomes. Interest rate effects and wealth effects played an important role as well (Chart E). At the same time, precautionary motives also had a positive impact on savings − particularly in 2022 following the Russian invasion of Ukraine, which led to a fall in consumer confidence. However, the importance of such motives seems to have decreased, as consumer confidence has gradually recovered from its slump in the second half of 2022.[12] Finally, the change in the saving rate over the past two years cannot be fully explained by the factors outlined above. This is highlighted by the unexplained part in the decomposition, which points to unmodeled factors that together have weighed on the increase in the saving rate since mid-2022. However, this cumulative perspective masks the fact that the increase in savings over the last three quarters was larger than previously anticipated and suggested by the model. This most likely reflects stronger consumption inertia and a more gradual adjustment of households’ spending to their increasing purchasing power and diminishing negative shocks than implied by historical regularities.[13]

Chart E

Contributions to the change in the household saving rate: a model-based decomposition

(percentage point changes since the second quarter of 2022 and percentage point contributions)

Sources: Eurostat, ECB, ECB and Eurostat (QSA) and ECB calculations.

Note: The chart shows the contributions of real household income, real net wealth, real interest rates and consumer confidence to the cumulative changes in the household saving rate since the second quarter of 2022, based on an estimated error correction model for private consumption growth and taking the growth in real household income as given.

Looking ahead, the household saving rate is likely to remain elevated in the near term but should decline below its current level further out. With the key factors – rising real incomes, elevated real interest rates and incentives to rebuild real wealth – likely to persist for some time, the saving rate is expected to remain high in the near term, albeit somewhat lower than its most recent peak, partly reflecting the moderating interest rates. The likely downtick in the saving rate together with continued strong growth in real labour income are expected to help the momentum of private consumption.

The quarterly sectors accounts (QSA) for the euro area are jointly compiled by the ECB and Eurostat.

See the box entitled “COVID-19 and the increase in household savings: precautionary or forced?”, Economic Bulletin, Issue 6, ECB, 2020.

See also the box entitled “A primer on measuring household income”, Economic Bulletin, Issue 8, ECB, 2023.

See, for example, Bańkowska, K. et al., “ECB Consumer Expectations Survey: an overview and first evaluation”, Occasional Paper Series, No 287, ECB, December 2021.

See the article entitled “Fiscal policy and high inflation”, Economic Bulletin, Issue 2, ECB, 2023.

See the boxes entitled “The impact of higher energy prices on services and goods consumption in the euro area”, Economic Bulletin, Issue 8, ECB, 2022, and “How have households adjusted their spending and saving behaviour to cope with high inflation?”, Economic Bulletin, Issue 2, ECB, 2024.

See the box entitled “Monetary policy and the recent slowdown in manufacturing and services”, Economic Bulletin, Issue 8, ECB, 2023.

See the box entitled “Household savings and wealth in the euro area – implications for private consumption”, Winter 2024 Economic Forecast, European Commission, 2024.

For a detailed analysis of the impact of inflation and monetary policy on the wealth distribution, see the article entitled “Introducing the Distributional Wealth Accounts for euro area households”, Economic Bulletin, Issue 5, ECB, 2024.

See also de Bondt, G., Gieseck, A., Herrero, P. and Zekaite, Z., “Disaggregate income and wealth effects in the largest euro area countries”, Working Paper Series, No 2343, ECB, December 2019.

The model parameters are estimated using data from the first quarter of 1999 to the last quarter of 2019. In order to obtain real values, household income and net wealth are deflated using the private consumption deflator from the national accounts. The real interest rate is measured by the three-month EURIBOR adjusted for the expected annual consumer price inflation rate from the European Commission’s consumer survey, which is backdated for the missing period from the first quarter of 1999 to the last quarter of 2003 using the actual annual HICP inflation rate. Consumer confidence is expressed in deviations from its long-term pre-pandemic average.

See the box entitled “Why are euro area households still gloomy and what are the implications for private consumption?”, Economic Bulletin, Issue 6, ECB, 2024.

Another factor which is not included in the model and may have contributed to the recently elevated saving rates relates to the high level of uncertainty about longer-term policy issues; see the box entitled “What are the economic signals from uncertainty measures?” in this issue of the Economic Bulletin.