Energy shocks, corporate investment and potential implications for future EU competitiveness

Published as part of the ECB Economic Bulletin, Issue 8/2024.

1 Introduction

The surge in energy prices following the unjustified Russian invasion of Ukraine exposed the EU to the largest energy shock since the 1970s. As a key input in virtually any production process, the sharp rise in energy prices not only contributed to a surge in inflation and a loss of purchasing power for households but also to a significant increase in input costs, with ripple effects across all economic sectors.

Shocks that increase the cost of energy can negatively influence economic dynamics not only in the short run but also in the medium to long run through the investment channel. In the short term, higher input costs put downward pressure on production.[1] This can also result in lower investment, with negative consequences for productivity growth in the long term.[2]

The economic literature has long identified the importance of investment for productivity. Corporate investment, especially in fixed capital and research and development (R&D), is at the heart of productivity growth, which is in turn directly linked to the ability of firms to compete in international markets.[3] Productivity improvements reduce the cost of production per unit of output, allowing firms to lower prices and/or increase profit margins. Productivity increases can also enhance export competitiveness, as more productive firms are better positioned to capture and expand their market share.[4]

Energy shocks can also dampen a country’s competitiveness through their negative impact on investment and productivity. Following a positive shock to energy costs, compressed profit margins (especially for energy-intensive firms), subdued economic activity, heightened uncertainty and, in some cases, tighter financing conditions may reduce investment by firms, paving the way for future competitiveness losses.[5] This may occur particularly when producers are unable to fully pass on the cost increases to consumers, for instance due to a high price elasticity of demand.[6]

However, energy shocks can also incentivise firms to invest in energy generation and energy-saving projects.[7] Recent surveys indicate that firms are adapting to the evolving energy landscape by reducing their dependence on traditional energy sources in order to shelter against future energy shocks and secure competitive advantages.[8] These efforts to reduce the energy bill can lead to an increase in green investment, which can mitigate the overall impact of energy shocks on total investment. However, despite their potential to mitigate future energy shocks (and to reduce future energy prices), green investments may also be adversely affected by the direct and indirect consequences of an increase in energy prices.[9]

This article explores how energy shocks influence investment by European firms, focusing on fixed capital and R&D expenditure. Empirical analysis shows that energy shocks can have a negative impact on corporate investment and thus, potentially, undermine European productivity growth and future competitiveness. The analysis also shows that financially constrained firms and firms in energy-intensive sectors are more affected by energy shocks and respond by cutting investment more than other firms.

From a policy perspective, both national and EU measures are needed to reduce the exposure of the EU to future energy shocks. Further integration of European energy markets and progress in the green transition would contribute to reducing energy prices and strengthening energy supply, making the EU less vulnerable to adverse energy price developments.

2 The European energy mix

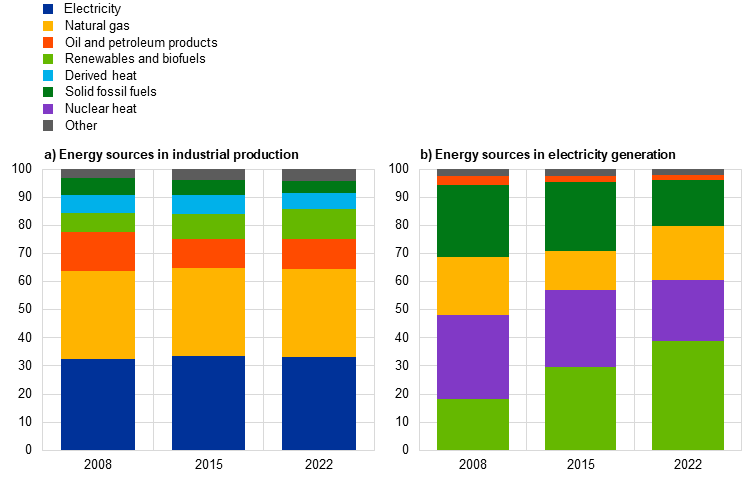

The main energy sources used in production in the EU are electricity and natural gas, together with oil and petroleum products. Electricity and natural gas are key inputs, each making up around a third of the EU’s industrial energy mix. These are followed by “oil and petroleum products” and “renewables and biofuels” at 11% each (Chart 1, panel a).[10] The industrial energy mix has remained largely unchanged over the past 15 years. When considering the energy landscape in which industry operates, it is also relevant to consider how the consumed electricity is generated, as this has a significant impact on its price. While the share of renewables in the EU electricity generation mix is growing, natural gas and other fossil fuels still play an important role (Chart 1, panel b), indirectly increasing their importance in the energy supply of firms.

Chart 1

Energy sources in industrial processes and electricity generation in the EU

(percentages)

Source: Eurostat.

Notes: Annual frequency. Panel a) refers to final consumption in the industrial sector. Panel b) refers to gross electricity generation. Oil and petroleum products exclude the biofuel portion. The category “other” includes manufactured gases, non-renewable waste, oil shale and oil sands, and peat and peat products.

Due to the marginal pricing system, the price of electricity is closely linked to fossil fuels. Electricity prices in short-term markets are determined by the most expensive facility used to generate electricity at any given point in time. In the EU, gas-fired power plants are typically the most expensive way of generating electricity, followed by coal, lignite and nuclear power. Renewables are typically the cheapest, as their variable costs are close to zero. A consequence of this mechanism is that gas often acts as the price-setter even though it generates a relatively low share of the EU’s electricity. According to the European Commission, in 2022 gas-fired power plants generated 19% of the EU’s electricity but set the price 55% of the time.[11]

Wholesale energy prices in the EU began rising significantly in the second half of 2021. As the EU imports nearly all the oil and gas it consumes, it is strongly exposed to price fluctuations in global markets, which can be affected by geopolitical developments and production decisions outside of the EU. Wholesale oil and gas prices started to go up in the second half of 2021, in part because of the recovery in economic activity following the pandemic and in part due to constraints in the supply of oil and gas. This was exacerbated by the Russian invasion of Ukraine in 2022, which drove up gas and oil prices further.[12] High gas prices had, in turn, a knock-on effect on electricity prices due to the marginal pricing system.

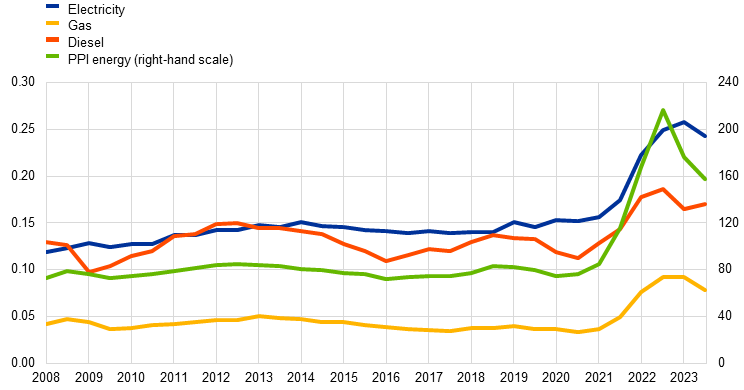

The spike in wholesale prices had a strong impact on the price of energy for EU industry. Wholesale prices are not transmitted perfectly to retail prices, as the latter are also influenced by factors such as taxation, regulatory frameworks, infrastructure availability, the electricity generation mix and contract structures. From 2021 onwards, many public policy measures were also taken to cushion energy shocks. Nevertheless, Chart 2 shows that the increase in wholesale prices was strongly transmitted to the retail prices paid by EU firms for electricity, natural gas and diesel. This had a significant impact on their production costs, with the producer price index for energy (PPI energy) more than doubling between 2020 and 2022.

Chart 2

Retail energy prices for firms in the EU

(left-hand scale: EUR/kWh; right-hand scale: index: 2021 = 100)

Sources: Eurostat and European Commission Oil Bulletin.

Notes: Frequency is semi-annual. Prices include all taxes and levies. For electricity and gas prices, data refer to medium-sized industrial consumers (band IC for electricity and I3 for gas). Gas prices for Cyprus and Malta are not included because Eurostat does not report the relevant data. As there is no Eurostat indicator for oil prices for non-household consumers, diesel is shown as an example of an oil product commonly used by EU industry, applying a conversion factor of 10 kWh per litre.

These developments spurred an intense policy debate about the EU’s dependence on imported energy and on the implications for its competitiveness in the face of energy shocks.[13] The EU relies significantly on imported energy and is thus more exposed to energy shocks than other major economies, such as the United States.[14]

3 The impact of energy shocks on EU corporate investment

While quantifying the effects of energy shocks on investment decisions is challenging, owing to the multitude of transmission channels as well as data limitations, exploring historical patterns can provide useful insights. To pin down the effect of energy shocks on investment, this article employs balance sheet data on publicly listed firms from Standard & Poor’s Compustat for the period 1999-2022 and estimates the response of fixed capital and R&D investment using local projections.[15]

Energy shocks can originate from different energy sources, and correctly identifying them is a major challenge. The energy crisis of 2022 was triggered by the disruption of natural gas supplies in Europe, which led to an increase in fossil fuel and electricity prices. However, given the historical importance of oil shocks, these have attracted more attention from academic literature than gas shocks, resulting in only a few reliable and readily available measures for the latter.[16] Furthermore, oil accounts for a significant share of energy consumed by the EU industrial sector, and prices of other energy sources, such as gas, are influenced by oil prices. Oil shocks can therefore be a good proxy for energy shocks, albeit with some caveats.[17] One of the most recent methods for identifying and measuring oil shocks concerns oil supply news shocks.[18] These shocks capture shifts in expectations about future oil production and prices rather than immediate disruptions, making them particularly relevant for investment decisions.[19]

Oil supply news shocks increase energy prices and reduce aggregate investment. As shown in Chart 3, an oil supply news shock leads to a contemporaneous increase of 7% in oil prices and of 1% in PPI energy.[20] Moreover, total gross fixed capital formation (GFCF) declines immediately after the shock, reaching a trough of -1.5% after two years. Investment in intellectual property products (IPP), which includes R&D, also decreases by 1% two years after the shock.[21]

Chart 3

Impact of oil supply news shocks on aggregate variables

a) Impact on oil prices and PPI energy | b) Impact on GFCF and IPP |

|---|---|

(x-axis: years; y-axis: percentage changes) | (x-axis: years; y-axis: percentage changes) |

|  |

Sources: Eurostat and ECB calculations.

Notes: The panels illustrate local projection estimation results on macroeconomic aggregates. The data for all regressions span the period from the first quarter of 1999 to the third quarter of 2023. For oil prices, the regression specification follows: . PPI energy (index), GFCF (real 2015 EUR) and IPP (real 2015 EUR) include panel data for EU28 countries and the specification follows , where is the outcome variable of interest at horizon h for country j, and includes a set of macroeconomic controls, including the lagged dependent variable. The shock is normalised such that it increases PPI energy by 1% on impact. The solid lines show the estimated impulse responses, while the shaded areas represent 90% confidence intervals based on Newey-West standard errors robust to serial correlation (for oil prices) or Driscoll-Kraay standard errors robust to serial correlation and cross-section dependence.

Consistent with the aggregate evidence, firm-level analysis based on publicly listed firms shows that oil supply news shocks exert downward pressure on investment.[22] As shown in panel a) of Chart 4, following an oil supply news shock that increases PPI energy by 1%, capital expenditure of publicly listed firms decreases by 2.9% on impact and 4.1% after one year.[23] R&D expenditure displays a smaller decline of around 0.85% both on impact and one year after the oil shock (Chart 4, panel b). Compared to the aggregate analysis, firm-level results show a larger impact of the shocks on capital expenditure and a similar impact on R&D expenditure. A possible explanation for this discrepancy lies in the sample coverage. In the Compustat sample analysed, R&D expenditure accounts for approximately 60% of aggregate R&D spending on average during the sample period. In contrast, the sample coverage for capital expenditure is only around 20%. This suggests that the firm-level R&D response is likely to be more aligned with the aggregate results than the capital expenditure response. However, the exact nature of the difference in terms of capital expenditure is not known beforehand, meaning that the response could be either larger or smaller than the aggregate result. Examining the sectoral coverage reveals that energy-intensive firms are represented more in the firm-level sample than in the aggregated data. Specifically, the capital expenditure of energy-intensive firms makes up about 40% of total capital expenditure in the Compustat sample, whereas it only accounts for 12% in the aggregate data.[24] To the extent that energy-intensive firms are more susceptible to energy shocks and hence reduce investment more than non-energy-intensive firms, the firm-level results are consistent with the aggregate findings. This is discussed in more detail in the next paragraph.

Chart 4

Impact of oil supply news shocks on firms’ fixed capital and R&D expenditure

a) Impact on fixed capital expenditure | b) Impact on R&D expenditure |

|---|---|

(x-axis: years; y-axis: percentage changes) | (x-axis: years; y-axis: percentage changes) |

|  |

Source: ECB calculations.

Notes: Data cover publicly listed firms from Standard and Poor’s Compustat Global incorporated in EU28 countries over the period 1999-2022. Financial and utilities sectors are excluded. The econometric specification closely follows Cloyne, J. et al., “Monetary Policy, Corporate Finance, and Investment”, Journal of the European Economic Association, Vol. 21, No 6, 2023, pp. 2586-2634, which uses state-dependent local projections (see Jordà, Ò. and Taylor, A.M., “Local Projections”, NBER Working Paper, No 32822, August 2024) to estimate the response of corporate investment to a monetary policy shock. We estimate the effects of oil supply news shocks (S) on long-difference percentage changes in firm-level capital and R&D expenditure (Y), accounting for firm characteristics that drive the overall effect: .

The state-dependent local projections extend over a horizon of three years after the oil shock, with firm-level fixed effects and standard errors clustered at the firm and time level following Driscoll-Kraay. Matrix X includes controls for the lagged real assets of the firm, its equity to debt ratio, its liquidity ratio (defined as liquid assets over total liabilities), profit margin, sales growth and the GDP growth of the country where it is located, along with the corresponding central bank policy rate. The shock is normalised such that it increases PPI energy by 1% on impact.

The solid lines show the estimated impulse responses, while the shaded areas show the 90% confidence intervals.

The role played by energy intensity warrants consideration because energy-intensive industries (EIIs) are particularly vulnerable to energy shocks owing to their energy needs. EIIs include sectors such as chemicals, metals, cement and glass and account for about 45% of electricity, gas and oil used by EU industries, despite representing less than 4% of EU gross value added in 2021.[25] These provide key materials for industries such as construction, the automotive industry and electronics and are important suppliers to sectors driving the green and digital transitions.[26] As a result, these are pivotal both to the EU’s decarbonisation goals and to its open strategic autonomy. However, European EIIs are burdened with electricity prices that are significantly higher than in some other economies, such as the United States, resulting in a competitive disadvantage.[27]

Financial constraints also play an important role in the investment decisions of firms. Financing conditions have long been recognised in the academic literature as critical enablers of investment, significantly influencing firms’ capacity to respond to shocks.[28] Survey evidence further indicates that financial constraints frequently emerge as major barriers to investment, particularly during periods of economic uncertainty.[29] Measuring financing constraints is challenging, as there is no agreed definition, but balance sheet data can be used to construct relevant estimates. The literature indicates that firms with relatively high debt (defined as a leverage ratio higher than the sample median) that are also of young age can be considered financially constrained.[30] High leverage constrains financing because firms with significant debt can be considered riskier, which leads to higher borrowing costs and stricter financing terms, while being a young firm compounds this constraint, as younger firms may lack established credit histories, collateral and proven revenue streams, making lenders more cautious when lending to them and thus limiting the availability of affordable external financing.

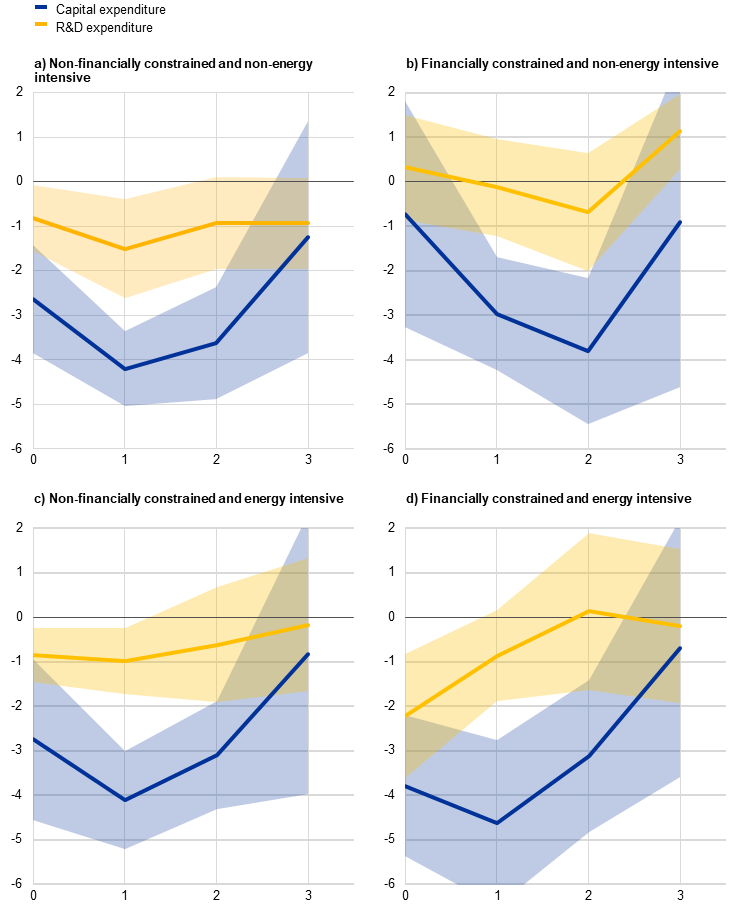

The joint occurrence of high energy intensity and financing constraints can amplify the effects of energy shocks. Recent survey data suggest that firms that self-identify as financially constrained are more likely to consider increases in energy costs as an impediment to investment than their non-financially constrained counterparts.[31] Empirical analysis reveals that financially constrained firms in energy-intensive sectors consistently reduce investment more sharply than other firms after an oil shock. Chart 5 shows the effect on firms, grouped according to energy intensity and financial constraints, of an oil supply news shock that raises PPI energy by 1% on impact. The analysis reveals that all groups reduce investment, but being in an energy-intensive sector and being financially constrained amplifies the impact of the shock on both capital and R&D expenditure.[32]

Chart 5

Impact of oil supply news shocks on capital and R&D expenditure by firm characteristics (energy intensity and financing constraints)

(x-axis: years; y-axis: percentage changes)

Source: ECB calculations.

Notes: For the econometric specification, see the notes to Chart 4. For the purposes of this analysis, financially constrained firms are those that are less than 20 years old and have a leverage ratio higher than the yearly sample median, which implies that whether a firm is financially constrained or not changes over time. The median was chosen to maximise observations per group, but results are robust to the choice of different thresholds. Energy-intensive firms are firms in NACE 2 sectors defined as EIIs by the European Commission.

The solid lines show the estimated impulse responses, while the shaded areas show the 90% confidence intervals.

4 Conclusion

The evidence presented in this article suggests that energy shocks tend to decrease investment and innovation in Europe, especially for financially constrained firms in energy-intensive sectors. Publicly listed firms in the EU reduce investment in response to energy shocks (as proxied by oil shocks). Empirical analysis indicates that a 1% increase in energy prices driven by oil shocks leads to a significant decrease in fixed capital expenditure (-4.1% after one year), while R&D spending drops by almost 1%, showing a more muted impact. Moreover, firms that are financially constrained and energy-intensive experience sharper reductions in investment following an oil price increase.

These findings are in line with a broad body of literature documenting the negative macroeconomic effects of oil shocks and confirm the importance of reducing the EU’s vulnerability to such shocks. The EU is heavily reliant on imported energy, making it more exposed to energy shocks than other major economies. As energy shocks put downward pressure on investment, and to the extent that investment slowdowns can lead to a decline in productivity, the EU is at risk of gradually losing competitiveness. This may threaten not only current but also future prosperity.[33]

Policy measures at both national and European level should therefore aim to secure the energy supply of the EU, lower energy prices and mitigate the exposure of firms to future energy shocks. While national interventions are best suited to address country-specific issues, EU actions should be aimed at tackling shared problems and fostering cross-country collaboration. The Draghi and Letta reports contain several proposals to address these issues.[34] These include strengthening joint procurement of gas imports to increase the EU’s market power and expanding the use of long-term electricity contracts. The two reports also emphasise that accelerating and simplifying permitting processes, channelling EU funds, and promoting cross-border projects to boost renewable energy production would enhance energy security and reduce energy prices in the medium term. Moreover, the Draghi report suggests targeted support measures for EIIs to ensure they remain competitive while contributing to decarbonisation. Finally, advancing the capital markets union could help ease financing constraints for firms, enabling them to invest in improving their energy efficiency. Together, these measures would have the potential to strengthen the resilience of the EU to future shocks and increase its long-term competitiveness.

See Lardic, S. and Mignon, V., “The impact of oil prices on GDP in European countries: An empirical investigation based on asymmetric cointegration”, Energy Policy, Vol. 34(18), December 2006, pp. 3910-3915.

Evidence presented in the article entitled “The impact of recent shocks and ongoing structural changes on euro area productivity growth”, Economic Bulletin, Issue 2, ECB, 2024, also shows that higher energy prices can lead to a reduction in productivity owing to the reallocation of factors of production within firms away from energy.

See Romer, P.M., “Increasing Returns and Long-Run Growth”, Journal of Political Economy, Vol. 94, No 5, 1986, pp. 1002-1037; and Romer, P.M., “Endogenous Technological Change”, Journal of Political Economy, Vol. 98, No 5, Part 2, 1990, pp. S71-S102.

See Melitz, M.J., “The Impact of Trade on Intra-Industry Reallocations and Aggregate Industry Productivity”, Econometrica, Vol. 71, No 6, November 2003, pp. 1695-1725.

See Lee, K., Kang, W. and Ratti, R.A., “Oil Price Shocks, Firm Uncertainty, And Investment”, Macroeconomic Dynamics, Vol. 15, No S3, November 2011, pp. 416-436.

See Matzner, A. and Steininger, L., “Firms’ heterogeneous (and unintended) investment response to carbon price increases”, Working Paper Series, No 2958, ECB, July 2024.

See Hassler, J., Krusell, P. and Olovsson, C., “Directed Technical Change as a Response to Natural Resource Scarcity”, Journal of Political Economy, Vol. 129, No 11, November 2021, pp. 3039-3072.

See “EIB Investment Survey 2023 – European Union overview”, European Investment Bank, October 2023; and “EIB Investment Survey 2024 – European Union overview”, European Investment Bank, October 2024.

See Bijnens, G., Duprez, C. and Hutchinson, J., “Obstacles to the greening of energy-intensive industries”, The ECB Blog, ECB, 17 September 2024.

The oil and petroleum products most commonly used by industry are gas oil and diesel oil, while the renewables and biofuels most commonly used by industry are solid biofuels such as wood.

See Gasparella, A., Koolen, D. and Zucker, A., “The Merit Order and Price-Setting Dynamics in European Electricity Markets”, JRC134300, European Commission, 2023.

See the article entitled “Energy price developments in and out of the COVID-19 pandemic – from commodity prices to consumer prices”, Economic Bulletin, Issue 4, ECB, 2022; and the article entitled “Geopolitical risk and oil prices” , Economic Bulletin, Issue 8, ECB, 2023.

See Draghi, M., “The future of European competitiveness”, September 2024.

For example, in 2022 the EU was reliant on imports for 62.5% of its energy needs. Import dependency was particularly high for natural gas (97.6%) and oil and petroleum products (97.7%). In contrast, the United States was a net energy exporter. See “Energy statistics – an overview”, Eurostat, May 2024; and “U.S. energy facts explained”, US Energy Information Administration, July 2024.

Over the period, investment by Compustat firms was on average equivalent to approximately 20% of total gross fixed capital formation and 55% of R&D investment at the European level.

See Hamilton, J.D., “This is what happened to the oil price-macroeconomy relationship”, Journal of Monetary Economics, Vol. 38, No 2, October 1966, pp. 215-220; and Raduzzi, R. and Ribba, A., “The macroeconomics outcome of oil shocks in the small Eurozone economies”, The World Economy, Vol. 43, No 1, January 2020, pp. 191-211.

Until 2015 the oil and gas markets were strongly linked. While they have gradually been decoupling in Europe since 2015, as the degree of indexation of gas contracts to oil prices has decreased, several studies suggest that such decoupling is not structurally complete. See the article entitled “Energy price developments in and out of the COVID-19 pandemic – from commodity prices to consumer prices”, op. cit.; Szafranek, K. and Rubaszek, M., “Have European natural gas prices decoupled from crude oil prices? Evidence from TVP-VAR analysis”, Studies in Nonlinear Dynamics & Econometrics, Vol. 28, No 3, June 2024, pp. 507-530; and Zhang, D. and Ji, Q., “Further evidence on the debate of oil-gas price decoupling: A long memory approach”, Energy Policy, Vol. 113, February 2018, pp. 68-75.

See Känzig, D.R., “The Macroeconomic Effects of Oil Supply News: Evidence from OPEC Announcements”, American Economic Review, Vol. 111, No 4, April 2021, pp. 1092-1125. Känzig proposes a novel method for identifying and quantifying oil supply news shocks by exploiting the high-frequency variation in oil futures prices surrounding OPEC announcements.

Alternative ways to identify oil supply shocks range from using a narrative shock series to structured vector autoregressions (VARs) identified with sign restrictions. See, for instance, Caldara, D., Cavallo, M. and Iacoviello, M., “Oil price elasticities and oil price fluctuations”, Journal of Monetary Economics, Vol. 103(C), May 2019, pp. 1-20; and Kilian, L., “Not All Oil Price Shocks Are Alike: Disentangling Demand and Supply Shocks in the Crude Oil Market”, American Economic Review, Vol. 99, No 3, June 2009, pp. 1053-1069. However, these measures lack the forward-looking dimension that characterises oil news shocks.

The shock is identified using instrumental variables within a VAR; hence it is identified up to sign and scale. To facilitate the interpretation of the results, in the article the oil supply news shock series is normalised to increase PPI energy by 1% on impact, which corresponds to a shock size of slightly above one standard deviation.

IPP pertains to investment in intangible assets, including R&D, software and databases, mineral exploration, and entertainment, literary and artistic originals.

The results are robust to the exclusion of the pandemic and the recent energy crisis, namely data after 2020.

Capital expenditure pertains to long-term fixed assets owned by companies and used to produce goods or provide services, including land, buildings, machinery, vehicles and equipment.

Not every country in the sample reports fixed capital expenditure at NACE 2 level, which is required to distinguish between energy-intensive and non-energy-intensive sectors. Therefore, the figure of 12% is calculated only on the sub-sample of countries for which this information is available, namely: Belgium, Bulgaria, Czech Republic, Denmark, Greece, Cyprus, Latvia, Hungary, Austria, Portugal, Romania, Slovakia, Finland, Sweden, Norway and the United Kingdom.

According to the European Commission’s Annual Single Market Report 2021, EIIs encompass several manufacturing sectors, including wood and wood products (excluding furniture), straw and plaiting materials, paper and paper products, coke and refined petroleum, chemicals and chemical products, rubber and plastic products, other non-metallic mineral products and basic metals.

For instance, every €100 of downstream private sector production contains on average €5 of inputs from chemicals, minerals and basic metals (see Draghi, M., op. cit.).

See Dashboard for energy prices in the EU and main trading partners 2023, European Commission. For example, between 2020 and mid-2022 the retail prices of electricity and natural gas (excluding recoverable taxes and levies) for EU firms were, on average, more than double the prices paid by their US counterparts. The retail price of diesel (including taxes) in the EU was slightly less than double the price in the United States.

For an overview, see Cloyne, J., Ferreira, C., Froemel, M. and Surico, P., “Monetary Policy, Corporate Finance, and Investment”, Journal of the European Economic Association, Vol. 21, No 6, December 2023, pp. 2586-2634.

See “EIB Investment Survey 2024 – European Union overview”, op. cit.

See, for example, Durante, E., Ferrando, A. and Vermeulen, P., “Monetary policy, investment and firm heterogeneity”, European Economic Review, Vol. 148, 104251, 2022; and Cloyne, J. et al., op. cit.

See “EIB Investment Survey 2023 – European Union overview”, op. cit.

The difference between the groups in panels a) and d) in Chart 5 is statistically significant on impact and after one year.

See Draghi, M., op. cit.

See Letta, E., “Much More Than a Market – Speed, Security, Solidarity: Empowering the Single Market to deliver a sustainable future and prosperity for all EU Citizens”, April 2024; and Draghi, M., op. cit.